v2.4.0-testnet Hardfork Upgrade Announcement")

Not every startup collapse is an FTX or Theranos. They don’t all burn so brightly and explode so spectacularly. More often than not, there won’t be some high-profile court case and prison time. Amanda Seyfried isn’t going to play you in the made for Hulu movie.

The story of most startup failures is far less exciting. The timing isn’t right, funding dries up, runways run out. Of late, a lot of macroeconomic factors have come into play, as well. These past few years have been especially brutal for startup land. According to a recent PitchBook survey, “approximately 3,200 private venture-backed U.S. companies have gone out of business this year.”

Combined, those companies raised north of $27 billion. Even more starkly, it’s a figure that doesn’t include companies that failed after going public or were able to find a buyer. That, after all, would really be stretching the definition of a “startup.”

It’s worth noting, too, that “failure” is subjective. Does bankruptcy qualify? It’s certainly not a good sign with regard to your company’s health, but plenty of companies have managed to bounce back to some degree. This particular question has been cause for plenty of discussion around the old TechCrunch virtual watercooler.

For the sake of a piece titled “The Startups We Lost,” I’ve opted to limit the list to those startups that — to the best of our knowledge — have hit the point of no return. Pushing up daisies. Pining for the fjords.

As the final days fall off the calendar, let’s take a moment to remember some of the startups that didn’t make it.

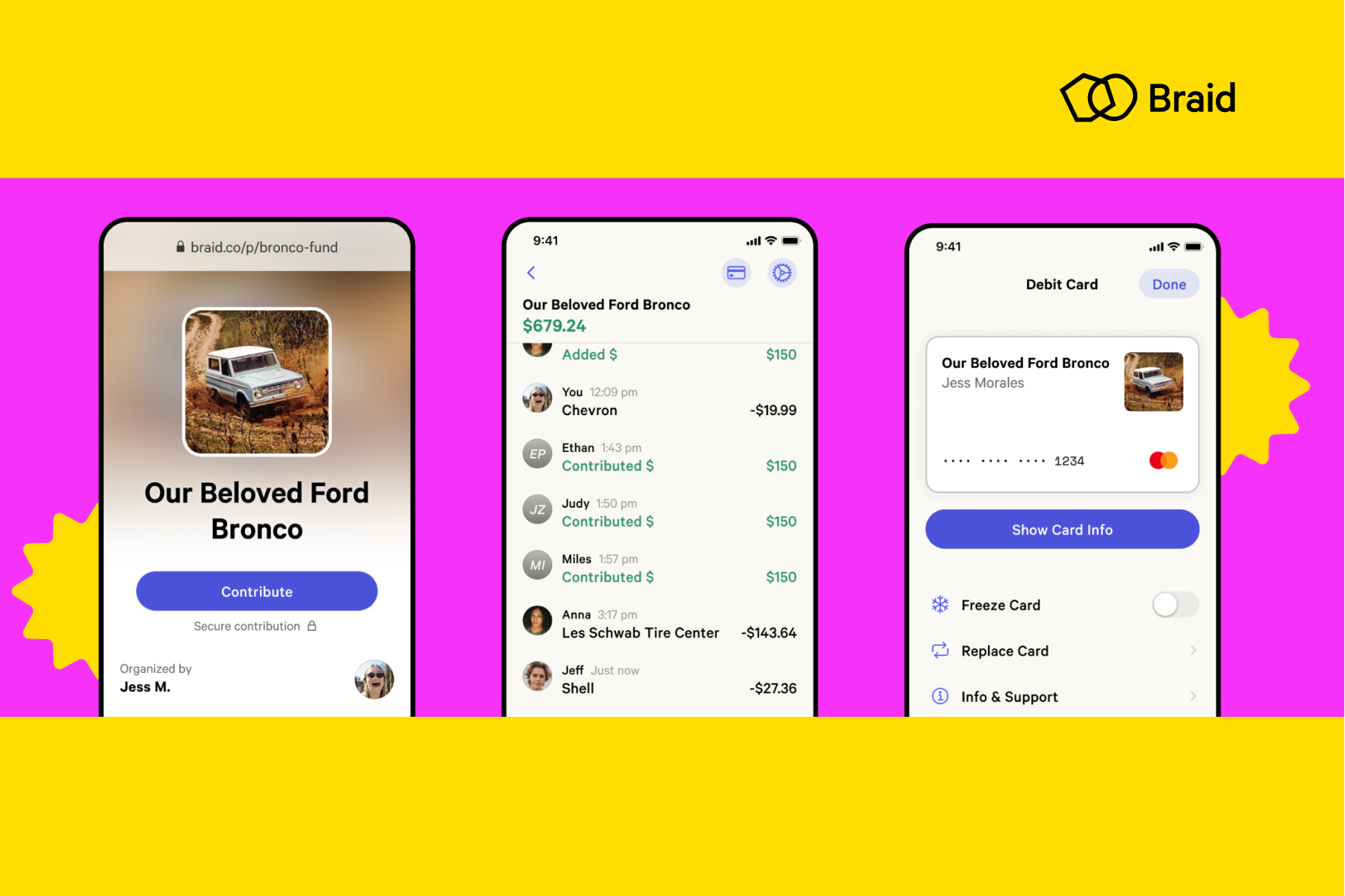

Braid

Founded 2019

$600 million raised

Image Credits: Braid

In October, Braid, a four-year-old startup that aimed to make shared wallets more mainstream among consumers, announced it had shut down. Founded in January 2019 by Amanda Peyton and Todd Berman (who left in 2020), San Francisco-based Braid set out to offer friends and family an FDIC-insured, multiuser account that was designed to make it easy “to pool, manage and spend money together.” Braid raised a total of $10 million in funding “over multiple rounds” from Index Ventures, Accel and others.

What was refreshing about this closure was Peyton’s candor about what led to Braid’s demise. In a blog post, Peyton said that Braid had closed its doors in September, and outlined her experiences — and mistakes — in building the company, ultimately realizing that it wasn’t going to be a viable business venture. An estimated 91% of startups fail. If more founders shared their experience like Peyton did so others could learn from them, maybe that number would go down.

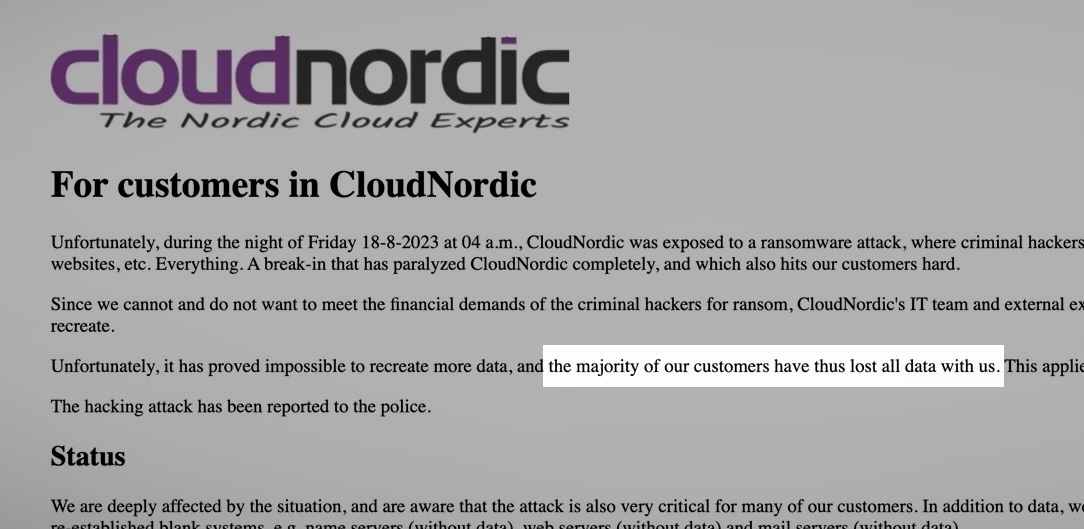

CloudNordic

Founded 2007

Image Credits: TechCrunch (screenshot)

CloudNordic might not be a household name, but a destructive ransomware attack on its systems propelled the company into the limelight — and its ultimate demise. The Danish cloud host provider shut down this year after close to two decades of operation following a ransomware attack that wiped out the company’s systems and destroyed all of its customers’ data. The company said it didn’t have the money to pay the hackers, and wouldn’t even if it did. With no options left, the company closed its doors.

Convoy

Founded 2015

More than $1 billion raised

Image Credits: Convoy

The digital freight broker abruptly closed in October 2023, just eight months after the Seattle-based company raised $260 million in fresh funding that pushed its valuation to $3.8 billion. Convoy, founded by former Amazon and Google exec CEO Dan Lewis and CTO Grant Goodale, will live on — sort of.

Supply chain logistics platform Flexport acquired the assets of the shuttered digital freight network with plans to restore Convoy’s trucking logistics services for customers. Flexport didn’t acquire the business or any of its liabilities, but its CEO said it did plan to retain “a small group of team members from their core product and engineering team.”

Daylight

Founded 2020

$20 million raised

Image Credits: Daylight

In May 2023, Daylight, an LGBTQ+ banking platform that had raised $20 million in funding, announced it would be shutting down and ceasing operations on June 30. The announcement came months after NY Magazine published an explosive feature on the neobank. The article honed in on Daylight, whose seed and Series A fundraises TechCrunch had covered here and here, respectively. NY Mag’s piece detailed a lawsuit brought on by three former employees as well as alleged fabrications and inappropriate behavior on the part of co-founder and CEO Rob Curtis.

In a blog published in May, Curtis said he felt like “now is the right time to exit this market.” We heard in October that the suits had been dismissed by a federal court and that Daylight was acquired, but Curtis declined to comment further when we reached out. It was a disappointing outcome but one that highlighted the challenges of neobanks that target specific demographics. At the onset of the COVID-19 pandemic, we saw a flurry of such startups raising money, but since then, things have been relatively quiet. Part of the challenge is providing differentiated services that are actually unique to a certain community. Since Daylight’s closure, Curtis has moved on to a tequila-related venture.

Fuzzy

Founded 2016

$80 million raised

Image Credits: Fuzzy

Some startups die long, protracted deaths. Not Fuzzy. The pet care telehealth startup was here one day and gone the next. In February, the firm was reportedly hyping its growth on internal Zoom calls. Within months, the company had closed up shop. Fuzzy’s site was taken down without any warning issued to customers.

From the sound of things, even some top execs were left wondering precisely what had happened to the startup. That certainly hasn’t stopped the competition from attempting to capitalize on Fuzzy’s demise.

IRL

Founded 2016

$200 million raised

Image Credits: IRL

IRL’s meltdown was a hot mess. In 2022, the event organizing social app laid off one-quarter of its 100 or so employees. Co-founder and CEO Abraham Shafi put the blame on an extremely volatile market, while stating that the company’s cash runway would last at least until 2024. Then it shut down this June.

No social network is completely devoid of bots, but an internal investigation by its board of directors found that such accounts constituted around 95% of its 20 million active monthly users. In a lawsuit filed last month, IRL’s co-founders accused their investors of falsifying that figure in order to sabotage the firm, which was previously valued at $1.17 billion.

IronNet

Founded 2014

$400 million raised

IronNet founder Keith Alexander at TechCrunch Disrupt in 2017. Image Credits: Noam Galai / Getty Images

IronNet, founded by former NSA director Keith Alexander, was a once-promising cybersecurity startup, which at its peak raised more than $400 million in funding. But in the end, IronNet was no match for market forces (and poor leadership). After a bumpy ride going public and rounds of layoffs, Alexander departed as CEO in July and was replaced with the chairperson of the company’s largest investor. IronNet scrambled to stay afloat, but lasted only a few weeks longer before it laid off everyone else and filed for bankruptcy.

Mandolin

Founded 2020

$17 million raised

Image Credits: Mandolin (opens in a new window)

Plenty of startups struggled through the pandemic. Others thrived. Founded in June 2020, the concert livestreaming platform was the right startup at the right time. After all, it had only been a few months since venues across the U.S. closed their doors indefinitely. Mandolin’s subsequent rise was swift, taking on big name events with artists ranging from Lil’ Wayne to the Lumineers.

A year after its founding, the Indianapolis-based firm raised a $12 million Series A, following a $5 million seed round the previous October. In 2022, it seemed as though the platform was still thriving, even as venues across the country had re-opened. Mandolin diversified into other aspects of the live music experience, including venue partnerships and merchandizing.

This April, however, the startup announced on Instagram that it was closing up shop. “After 3 incredible years,” it noted, “we are sad to announce that Mandolin will no longer be offering the digital fan experiences you’ve come to love.”

Veev

Founded 2008

$597 million raised

Image Credits: Veev

Veev, a real estate developer turned tech-enabled prefab homebuilder, as of November was on the verge of shuttering after reaching unicorn status last year, according to multiple reports. Calcalist reported on November 26 that the company — which raised a staggering $600 million in total, $400 million of which was secured in March of 2022 — was going to have to close up shop after an “abrupt cancellation of a capital-raising initiative.” Later that week, it was reported that Veev was “undergoing liquidation.”

It was a bit of a shocking turn of events considering just how much money the company had raised not even two years prior. The closure was not the first startup failure for Veev co-founders Heller and Ami Avrahami. Another one of their proptech ventures, Reali, began a shutdown in August of 2022 after raising more than $290 million in debt and equity funding. Zeev Ventures was an investor in both companies.

ZestMoney

Founded 2015

$121 million raised

ZestMoney founders resign as Goldman Sachs-backed fintech struggles to raise funds. Image Credits: ZestMoney

In mid-May, Manish reported on the fact that founders of ZestMoney had resigned from the startup. The Indian fintech, whose ability to underwrite small ticket loans to first-time internet customers, once drew the backing of many high-profile investors, including Goldman Sachs. By December, Manish had reported that ZestMoney was shutting down following unsuccessful efforts to find a buyer.

The Bengaluru-headquartered startup — which also identified PayU, Quona, Zip, Omidyar Network and Ribbit Capital among its backers — employed about 150 people and had raised over $130 million in its eight-year journey.

Zume

Founded 2015

$445 million raised

Image Credits: Zume

“Pizza was our prototype,” co-founder and CEO Alex Garden told me in 2018. Three years after its founding, Zume made a major pivot. While it will forever be remembered as the pizza robot startup (that’s a hard identity to shake), the Southern Californian company cast a wider net. First it was exploring non-pizza delivery trucks. Two years later, it pivoted into sustainable food packaging.

Throughout its many lives, one certainly can’t pin Zume’s ultimate demise on a failure to adapt. Nor was it a lack of funding, as the company raised nearly half-a-billion in its eight-year history. That includes a 2018 SoftBank round of $325 million that valued the company at north of two billon.

Zume liquidated its assets in early June.

techcrunch.com