v2.4.0-testnet Hardfork Upgrade Announcement")

Data shows there’s hope amid the bleak headlines from this year

In the face of recent economic downturns and fears of a startup bubble-burst, it may be surprising to hear that startups are faring better than you might think. I’ve been talking to a bunch of founders who are struggling to raise funding — and that is a real problem — but there are some startups that focus on the business fundamentals that are still thriving.

A deep dive into the data from startup accounting firm Kruze Consulting shows that startups that can keep an eye on the fundamentals — that is, those that are running more like a “real” business, rather than the “growth at all costs” mentality we’ve seen over the last few years — are in pretty decent shape. Looking at the numbers, this presents as an uptick in median runway length, a decrease in operating expenses, and an encouraging rise in profitable revenue.

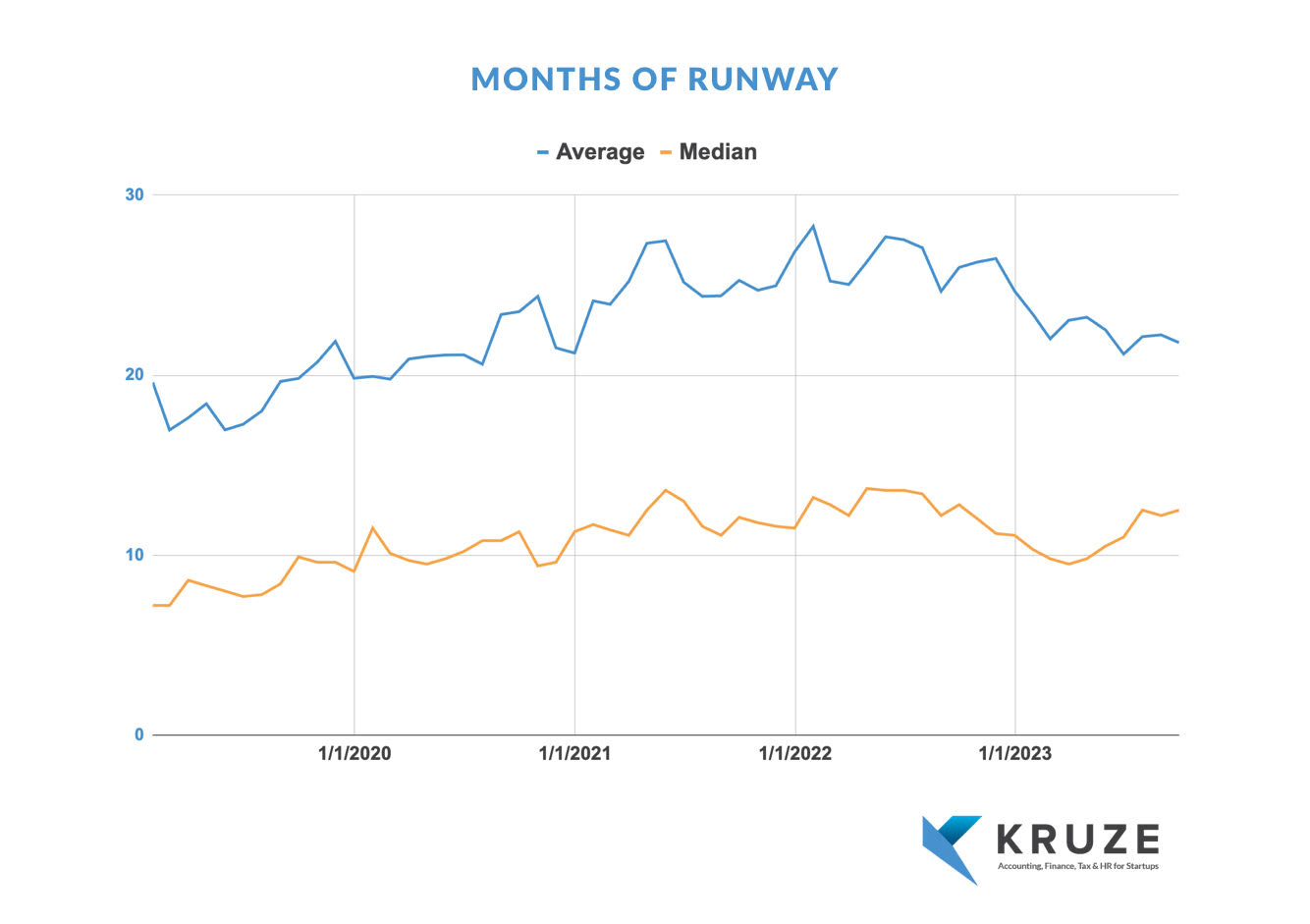

Running less lean than you’d think. Image Credits: Kruze Consulting

“The average burn is coming down this year, driven by lower OpEx spending. This is founders focusing on being more efficient,” Healy Jones, VP of financial strategy at Kruze Consulting, told me. “Of course, a lot of this is driven by the layoffs that have made headlines (so not a happy thing to brag about), but on the other hand, the founders are learning how to be more effective in using their cash, which is a good thing for the ecosystem.”

The median startup runway, which is the estimated amount of time a company can operate until it runs out of cash, has actually increased in the second half of 2023. It now stands at an impressive 12.5 months, significantly higher than the nine to 10 months usually expected after an average funding round.

techcrunch.com