v2.4.0-testnet Hardfork Upgrade Announcement")

[ad_1]

Bitcoin was last trading lower by over 3.0% on Friday in the low $23,000s, with BTC/USD falling back under its 21DMA for the first time in nearly two weeks in wake of a hotter-than-expected US Core PCE inflation report that raises the risk the US Federal Reserve lifts interest rates to higher levels for longer. MoM and YoY price pressures both unexpectedly rose in January, according to the latest report, to 0.6% and 4.7% respectively.

That has resulted in US money markets pricing in a 40% chance that the Fed will lift interest rates by at least 25 bps at its next four meetings. Prior to Friday’s data, the money market-implied odds for at least another four 25 bps in rate hikes over the course of the next four meetings was 30%. A month ago, markets assigned the likelihood of another 100 bps in rate hikes at roughly zero.

As a result, the US dollar is picking up, US yields are rising and US stocks have come under fresh selling pressure, a bearish combination for the risk-sensitive crypto asset class. Bitcoin traders will continue to monitor upcoming major US data releases and the tone of commentary from Fed officials as they continue to assess the outlook for US monetary policy.

But it seems that Fed tightening fears will continue to act as a near-term headwind for crypto. Indeed, Fed tightening fears have likely been the main factor behind Bitcoin’s recent pullback from earlier monthly highs in the low-$23,000s. But as the specter of a dip back towards the 50DMA in the $22,000 area and perhaps even a retest of recent lows in the $21,400 area looms, Bitcoin bulls can take solace in a few recent options market developments that suggest the 2023 bull market likely remains intact.

Bullish Options Market Signals

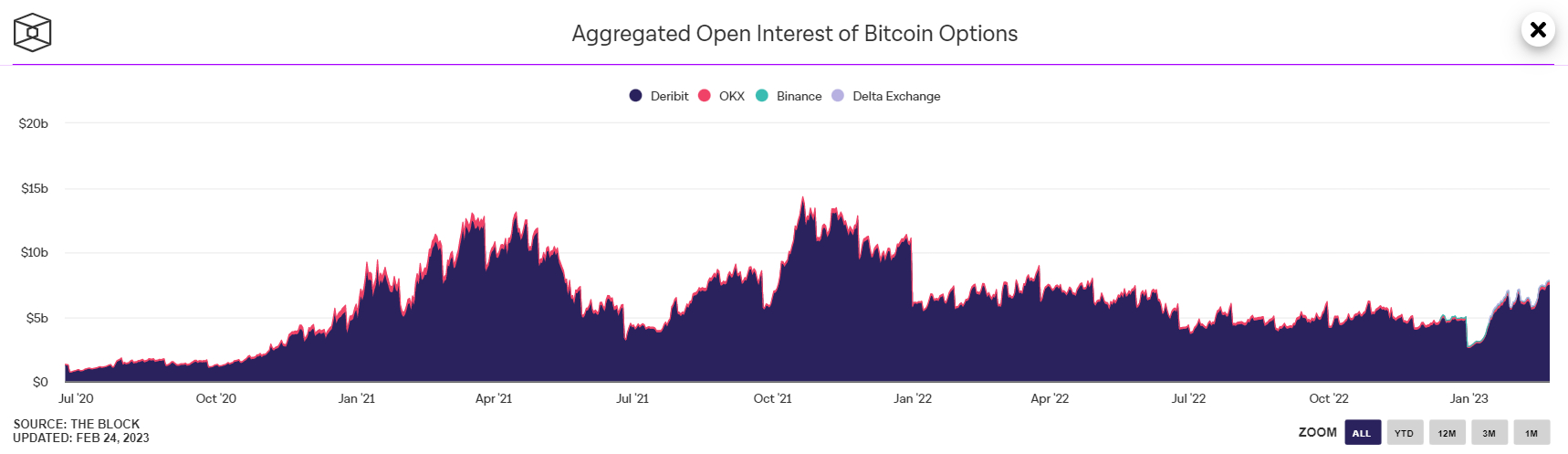

Aggregated Open Interest of Bitcoin Options (i.e. the aggregate value of existing options contracts) across major crypto derivative exchanges recently hit its highest level in nearly 10 months at $7.83 billion on Wednesday. Options are a more complex investment tool, typically used by a more “sophisticated” investor base for hedging and making price direction bets.

Hence, many view a rise in the Open Interest of Bitcoin Options as a sign that institutions are getting involved in the market once again. Institutional adoption has been an important narrative in past Bitcoin bulls markets and this narrative could definitely catch on once again if Open Interest makes further progress back to its 2021 record highs above $14 billion.

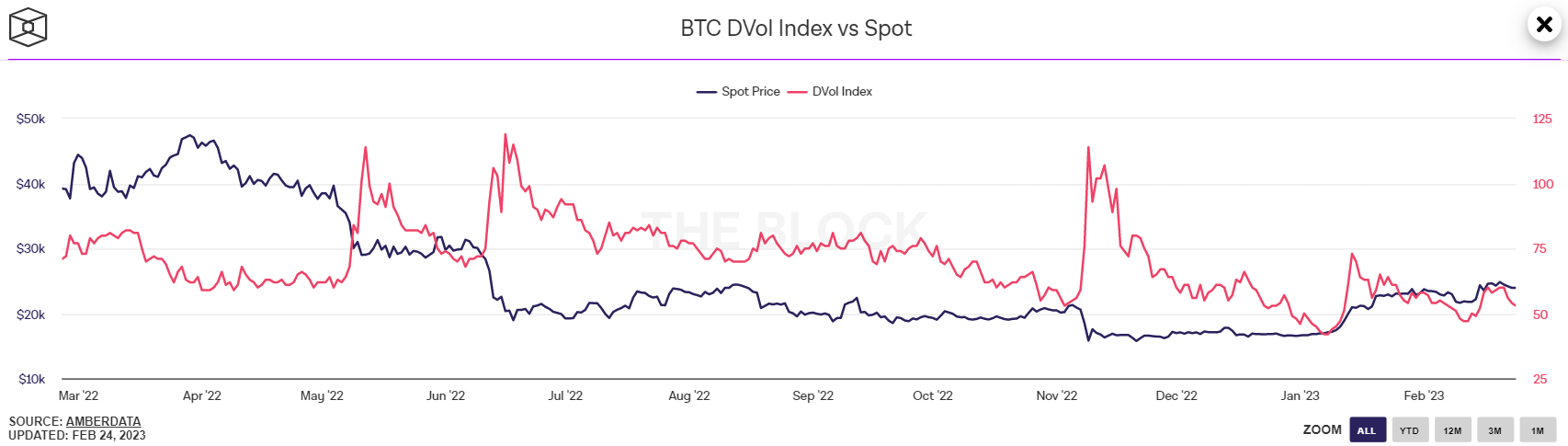

Elsewhere, Deribit’s Bitcoin Volatility Index (DVOL) remains close to all-time lows. It was last at 53 on Friday, down from earlier weekly highs at 60. That’s not too far above the record lows it printed earlier in the year at 43. The DVOL tends to spike at times of bearishness in the cryptocurrency market. Its ongoing stability is thus a reassuring signal.

Meanwhile, the 25% Delta Skew of Bitcoin Options expiring in 7, 30, 60, 90 and 180 days all remained slightly above zero on Friday, implying a still modestly positive market bias. Indeed, the 180-day 25% Delta Skew, last at 2.74, is only just under recent highs (the 3.28 printed in January) and is thus not far below its highest level in more than a year.

The 25% delta options skew is a popularly monitored proxy for the degree to which trading desks are over or undercharging for upside or downside protection via the put and call options they are selling to investors. Put options give an investor the right but not the obligation to sell an asset at a predetermined price, while a call option gives an investor the right but not the obligation to buy an asset at a predetermined price.

A 25% delta options skew above 0 suggests that desks are charging more for equivalent call options versus puts. This implies there is higher demand for calls versus puts, which can be interpreted as a bullish sign as investors are more eager to secure protection against (or bet on) a rise in prices.

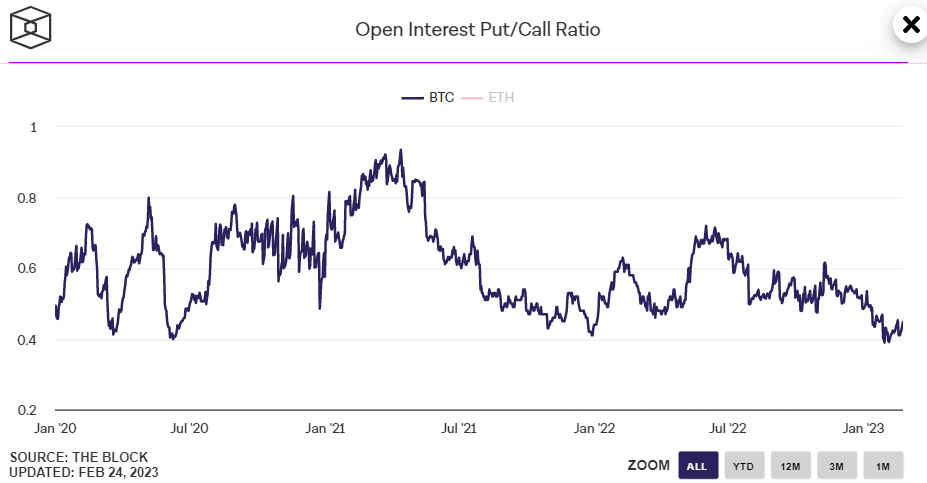

Finally, the ratio of Open Interest Put (bets on a price fall) vs Call (bets on a price rise) Options on Deribit remained close to its record low on Friday at 0.45. A record low was at the end of January under 0.40.

Elsewhere, as discussed in recent articles, a growing laundry list of on-chain and technical indicators all suggesting that the bear market is over. So whilst Bitcoin might not be able to maintain the pace of January’s rally, there are still a lot of reasons to think that a return to 2022’s lows remains unlikely.

[ad_2]

cryptonews.com