v2.4.0-testnet Hardfork Upgrade Announcement")

[ad_1]

Bitcoin has tried and failed to break and hold above the $25,000 level now for five out of the last six days. Some technicians think that this isn’t necessarily a bad thing, as the world’s largest cryptocurrency by market capitalization is forming an ascending triangle structure that could proceed an explosion higher towards the next major resistance area around $28,000.

But others are worrying that this year’s rally that has seen the BTC price already increase close to 50% may be stalling. Pricing in Bitcoin derivatives markets is one way to gauge how investors feel on the outlook for BTC, as well as towards its potential for volatility. Here’s what options markets are saying right now…

Investors Neutral on the BTC Price Outlook

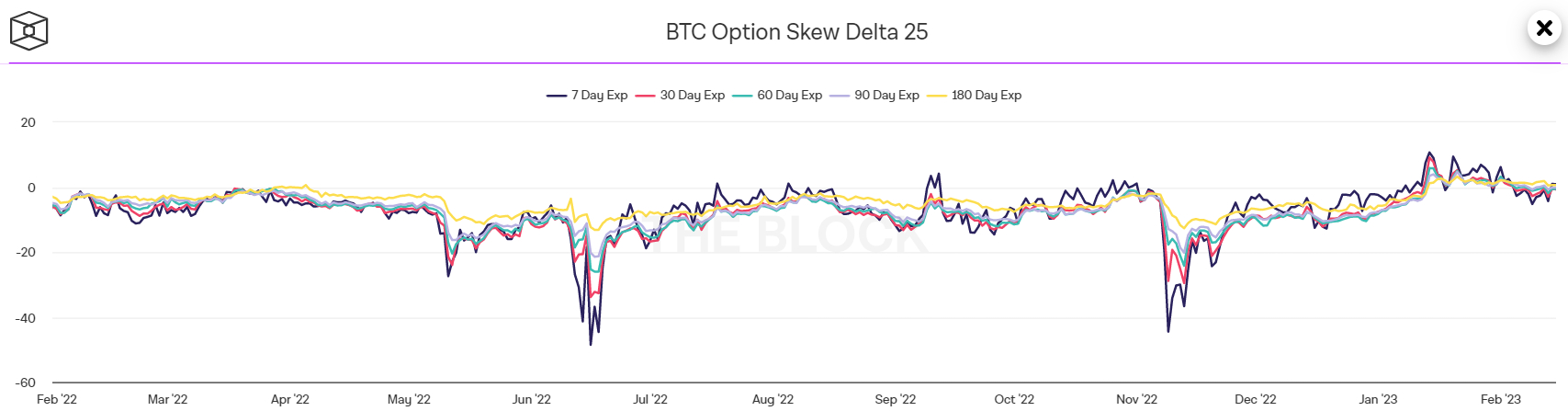

According to the widely followed 25% delta skew of Bitcoin options expiring in 7, 30, 60, 90 and 180 days, investors are currently roughly net neutral in their outlook for the Bitcoin price. According to data provided by crypto analytics firm The Block, all five 25% delta skews are close to zero, up substantially from last year’s immediate post-FTX collapse lows, but also down slightly from highs printed earlier this year in the year.

The 25% delta options skew is a popularly monitored proxy for the degree to which trading desks are over or undercharging for upside or downside protection via the put and call options they are selling to investors. Put options give an investor the right but not the obligation to sell an asset at a predetermined price, while a call option gives an investor the right but not the obligation to buy an asset at a predetermined price.

A 25% delta options skew above 0 suggests that desks are charging more for equivalent call options versus puts. This implies there is higher demand for calls versus puts, which can be interpreted as a bullish sign as investors are more eager to secure protection against (or bet on) a rise in prices.

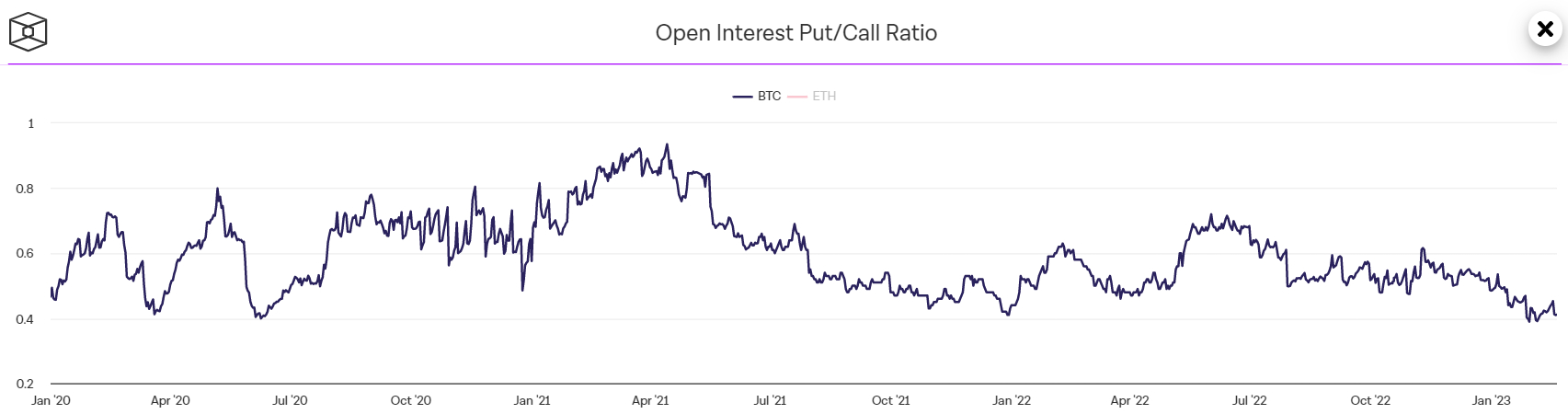

However, a separate option market indicator of investor sentiment is sending a more bullish sign. According to data presented by The Block, the Open Interest Put/Call Ratio of Bitcoin options was last at 0.41, still very close to the record lows printed in late January/early February. An Open Interest Put/Call Ratio below 1 means that investors favor owning call options (bets on the price rising) over put options (bets on the price dropping).

Investors Are Positioning For Uptick in Volatility

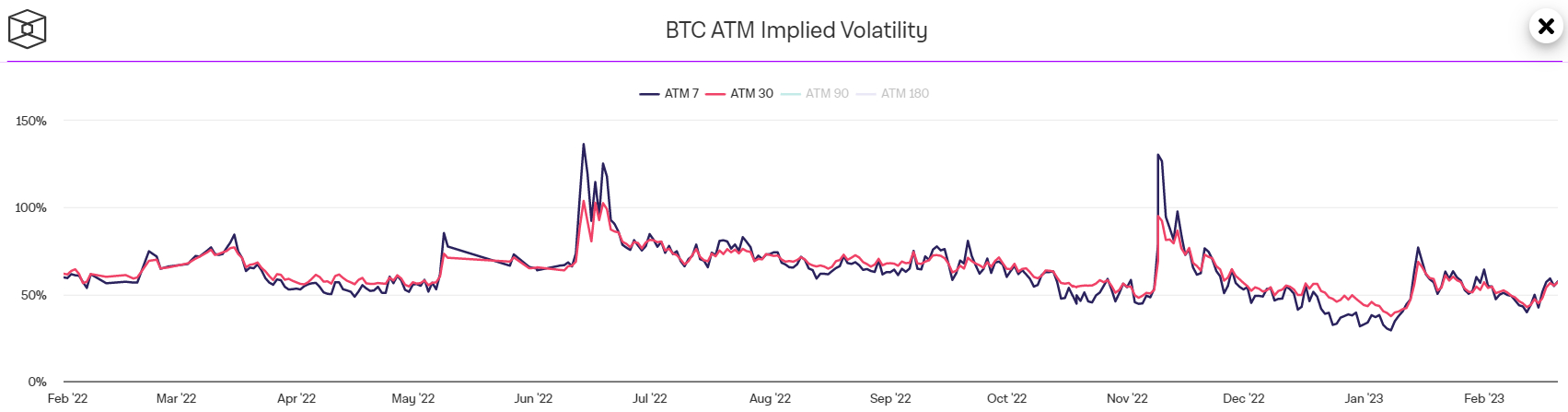

Bitcoin’s 7-day Implied Volatility according to At-The-Money (ATM) options market recently neared its highest level of the month, according to data presented by The Block. On Saturday, it rose to just under 60%, up from earlier monthly lows of below 40%. 30-day ATM Implied Volatility, meanwhile, was also at roughly 60% and in line with its earlier monthly highs.

The latest uptick in volatility expectations, as per ATM options markets, has gone hand in hand with the Bitcoin market’s recovery from earlier monthly lows in the $21,000s. It’s worth noting that, Bitcoin ATM Implied Volatility expectations remain subdued by historical comparison and well below recent mid-January 2023 and November 2022 highs.

[ad_2]

cryptonews.com